Background

On March 31, 2022, the SEC released Staff Accounting Bulletin No. 121 (SAB 121).

This SAB expresses the view of the SEC staff regarding the accounting treatment for crypto-assets that are reporting entity safeguards for its platform users (customer crypto-assets).

Exchanges that are responsible for safeguarding customer crypto-assets should present a liability on its balance sheet to reflect its obligation to safeguard the customer crypto-assets.

The exchange would recognize an asset at the same time it recognizes the safeguarding liability, measured at fair value at each reporting date.

Prior to the release of this SAB, it was not clear how entities should record customer crypto-assets under US GAAP.

For example, entities such as Coinbase did not record customer crypto-assets on its balance sheet.

The determination as to whether the custodian should record an asset and a related liability for crypto-assets it holds on behalf of its customers was dependent on an assessment of control over such assets and required the use of significant judgement based on the facts and circumstances.

With the release of SAB121, we can expect entities to start recording customer crypto-assets as a liability and a corresponding asset on their balance sheet.

A SAB is different from accounting standards released by the FASB (Financial Accounting Standards Board) in that they are not accounting standards, but are interpretations and views of the SEC staff.

Nonetheless, in practice, SABs are regularly referenced when determining accounting treatments and so are treated as quasi accounting standards.

Summary of SAB 121

Who is it applicable to?

Reporting entities that operate a platform that allows its users to transact in crypto-assets and that engages in activities in which it has an obligation to safeguard customers’ crypto-assets (ex. crypto exchanges).

What is the accounting treatment?

Record customer crypto-assets as a liability and a corresponding asset.

Both the liability and the asset are to be marked to market each reporting period.

When will SAB 121 be applicable?

In the first interim or annual financial statements ending after June 15, 2022 (i.e., Q2 2022 for calendar year-end public companies).

The guidance is required to be applied retrospectively to the beginning of the fiscal year in which the interim or annual period relates (i.e., January 1, 2022 for calendar year-end public companies).

Difference with Japan GAAP

With the release of SAB 121, the GAAP difference that existed regarding the treatment of customer crypto-assets is now gone.

The accounting guidance regarding crypto under Japan GAAP is prescribed in PITF (Practical Issues Task Force) No. 38 “Practical Solution on the Accounting for Virtual Currencies under the Payment Services Act”.

II-1-14 of the aforementioned PITF states the following regarding the accounting treatment for customer assets that exchanges custody on behalf of its users:

An asset is recognized at the market price when a virtual currency is deposited by a customer.

Furthermore, a liability representing an IOU is recorded, measured at the same amount as the asset.

Application of SAB 121 to Coinbase

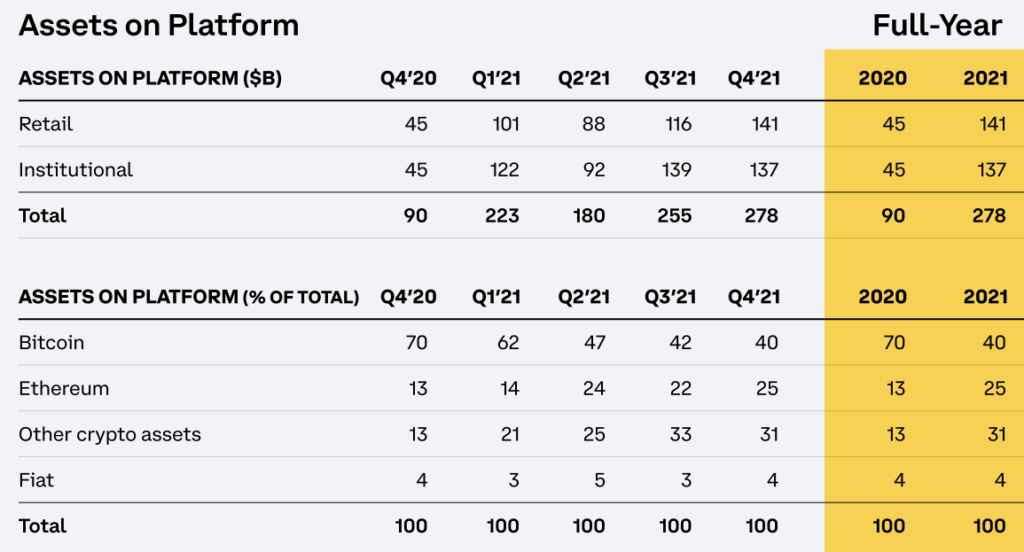

Page 10 of Coinbase’s FY2021 Shareholder Letter (February 24, 2022) has information regarding “Assets on Platform”, which appears to be the amount of customer crypto-assets Coinbase holds on behalf of its customers at the end of each quarter.

According to this information, the customer crypto-assets balance as of December 31, 2021 was 278 billion USD.

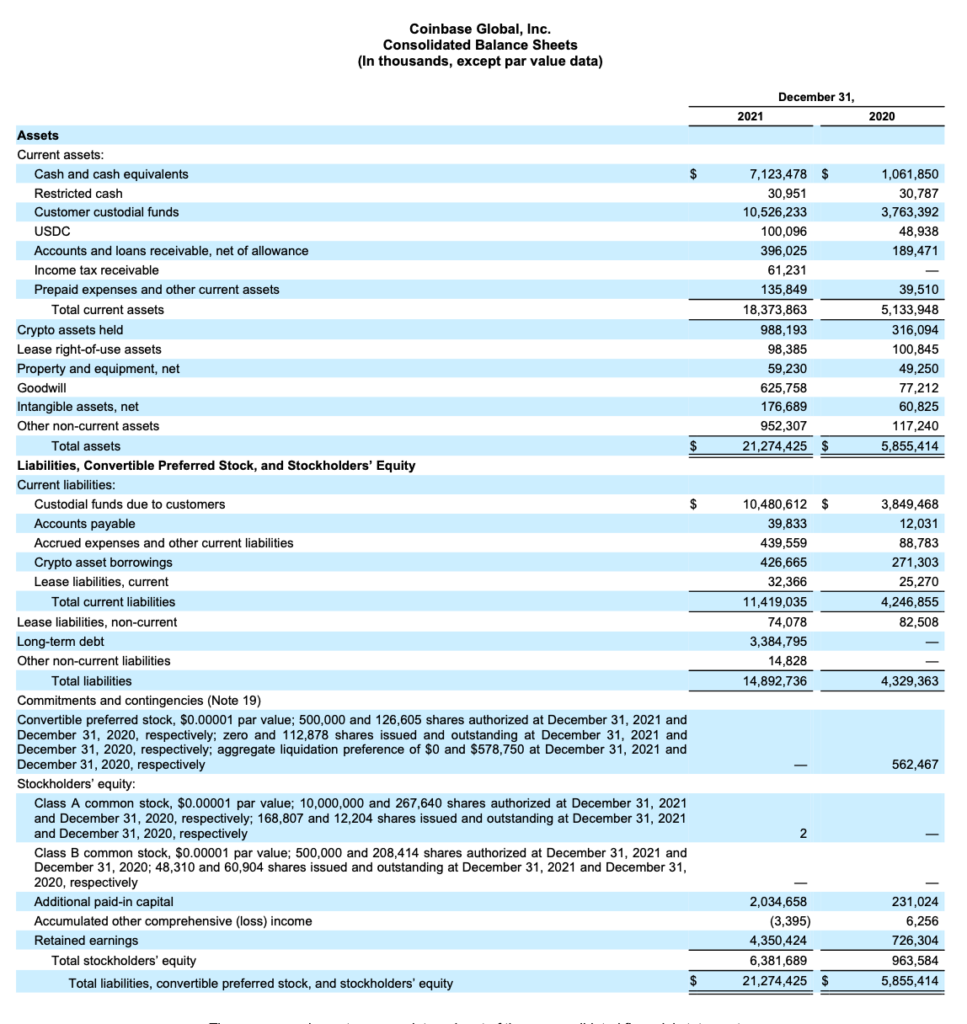

On the other hand, the balance sheet included in the 10-K for FY2021 shows total assets as of December 31, 2021 to be 21 biillion USD and is clear that the amount expected to represent customer crypto-assets is not recognized on the balance sheet.

SAB 121 becomes applicable during FY2022 Q2 for Coinbase, which means that one can expect Coinbase’s Q2 10-Q balance sheet to grow significantly larger.

Concerns regarding SAB 121 within the SEC

On the same day SAB 121 was released, SEC Commissioner Hester Peirce (aka Crypto Mom), who has held an open stance towards crypto in general, released a response addressing the SAB.

The response shows concerns in the way the change is being made, touching on the timing of the SAB release (why now), how the SAB is unusual in that it provides definitive interpretive guidance for a very specific, very limited number of public companies, and the granular disclosure guidance of the SAB.

Reference:

pwc: https://viewpoint.pwc.com/dt/us/en/pwc/in_briefs/assets/ib202206.pdf